China Credit Risk Mitigation.docx

《China Credit Risk Mitigation.docx》由会员分享,可在线阅读,更多相关《China Credit Risk Mitigation.docx(19页珍藏版)》请在冰点文库上搜索。

ChinaCreditRiskMitigation

China’sCreditRiskMitigationToolsPricingBasedonJarrow-TurnbullModel

WuMin,ZhangQiang*

(CollegeofFinanceandStatisticsofHunanUniversity,HunanChangsha,410079)

Abstract:

Creditriskmitigationtool(CRM)isaninnovativecreditriskmanagementtoolthatpilotlaunchedbytheinter-bankmarketin2010,itstrippingandpricingthecreditriskofcommercialpaper,medium-termnotes,bankloansandotherassets,andtransferredtherisktootherinvestment,theirintroductionradicallychangedthetraditionalfeaturesofcreditriskmanagement.First,thepricingofthepilotstatusofCRManalysis,theimpactoffactorsincludingCRMpricingrisk-freeinterestrate,theunderlyingbond'sriskexposure,defaultprobability,lossgivendefaultrateandduration,CRMdeadlines.Secondly,theintroductionofJarrow-Turnbullmodel,thepricingofcreditriskmitigationtoolstomeasureandfoundthatinterestratesorcentralbankbills,treasurybondsoverthesameperiodastheCRMbenchmarkinterestrateismoreappropriate,andtheJarrow-Turnbullmodelfordifferenttime,differentlevelsofCRMpricingofcreditdiscrimination.MorereasonabledealwiththeissueofpricingisclosertoCRM,CRMproductsforourcurrentpricing.Finally,proposeCRMpricingoptimizationstrategies,includingcompletingtheunderlyingdatabase,exploringRisk-freeinterestrate,innovativeunderlyingbondratingsystem,guidingCRMmarketdiversificationandoptimizationofmakertradingsystem.

Keywords:

Creditrisk;Riskmitigation;Riskpricing;Jarrow-TurnbullModel

Introduction

Bytheendof2010,thebalanceofChina’screditbondsreached4trillionRMB.Balanceofcommercialbankloansreached31.09trillion,10trillionofwhichgotocreditloans.Meanwhile,risksoffinancialproductslikebondsandloansarechangingfromsingleinterestrisktotwo-tierriskstructurecontainingbothinterestriskandcreditrisk.Becauseofthescarcityofcreditriskmanagementtools,itisdifficultforcommercialbanksandotherinstitutionalinvestorstoeffectivelyavoid,transfer,hedgerisksandoptimizeresourceallocationsandthereforereducesystemicrisks.Inthisoccasion,NationalAssociationofFinancialMarketInstitutionalInvestors(NAFMII)establishedtheChinaBondInsuranceCo.Ltd(CBIC),in2009,withthepurposeofdiversifyingcreditriskmanagementtoolsfortheinvestors,amelioratingcreditrisksharingmechanismandavoidingsystemicrisks.Between2010and2011,CBICcreatedproductslike“ChinaBondAgreementI”,“ChinaBondAgreementII”,“ChinaBondAgreementIII”and“ChinaBondAgreementIV”.CBICthusbecameoneoftheforerunnersinCRMcreationinChina’sfinancialmarketandthebiggestmarketmaker.InOct2010,NAFMIIofficiallyissuedthe“GuidelineforthepilotbusinessofCreditRiskMitigationinInter-bankMarket”,makingtheofficiallaunchoftheCRMpilotbusiness.

ThedevelopmentofCRMpilotbusinessisnotsmooth,though.FromNov2010whenCRMwasofficiallytradedtoMay2011,only9CreditRiskMitigationWarrants(CRMW)wereissuedbytheinter-bankmarket.InApril2011,completecancellationoftheCRMWissuedin2010(HSBCChinaCRMW001)byHSBCbeforehand,furtherworriedthebusinessandacademicsregardingthepilotbusinessofthisinnovativefinancialproduct.

1SurveyofResearchAtHomeandAbroad

1.1SurveyofResearchAbroad

Jarrow-TurnbullCreditRiskPricingModelinitiallyappearedinRobertJarrow&StuartTurnbull(1995)[1].LaterthatmodelwasappliedtothecalculationofBondDefaultRateandpricingofcreditproductslikeCreditDefaultSwaps(CDS).TheBaselCommittee(1999,2004)[2]firstintroducedtheconceptofCreditRiskMitigationatthebeginningofthe20thcentury,andgavethoroughintroductiontothetechnicalframework,coverage,mechanism,capitalchargeandinformationexposureofCRMindocumentsincluding“BaselNewCapitalAccord”and“InternationalConvergenceonCapitalMeasurementandCapitalStandard:

RevisedFramework”.Later,bystudyingtherelationshipbetweenCDSpricingandobjectbondyield,JohnHull,MirelaPredescu,andAlanWhite(2004)[3]etall,foundthattheCDSpricingriskfreebenchmarkinterestrateofCanadianCDSfallswithinthefive-yearaverageswapinterestrateandtheinterestrateofthetreasury.Bringingdowntheratingofobjectbondhassignificantinfluenceondefaultrateandpricechange,yetdowngradingandnegativelyprospectingitsdefaultrateandpricechangedoesn’thaveagreatinfluence.ChristianWeistroffer(2009)[4],Duquerroy&Gex(2009)[5],Ramacont(2010)[6]tooktheviewthatCRMprovidesmoreeffectivemeansofcreditmanagementforcostcontainmentofcommercialbanksandliquidityenhancement.Italsoprovidesnewinvestmentchannelsforinstitutionalinvestmentsandhelpsimprovetheefficiencyandstabilityoffinancialsystems.Garrett(2009)[7]pointedoutthattheadvantagesofCRMliesinfacilitatingcreditrisktransferandadjustmentofbalancesheets,whileitsdisadvantagesliesinthefactthat,CRMisbasicallyazero-sumgame,andcanonlytransfercreditrisks.InappropriateuseofCRMislikelytorepeatthetragediesofAIGandLehmanBrothers.Stulz(2010)[8]studiedtheinfluenceofCRMoncompanyandsubprimemortgage,andarguedthatthefundamentalcauseofthecurrentfinancialcrisisliesinthelackofexpectationofinvestorsandfinancialinstitutionsonassetpricefall,aswellastheexcessleverageoffinancialinstitutions.CDS,tothecontrary,issymptomratherthancauseofthecrisis.

1.2SurveyofResearchAbroad

AccordingtotheGuidelinepublishedbyNAFMII(2010),China’sCRMincludesCreditRiskMitigationAgreements(CRMA),CreditRiskMitigationWarrants(CRMW)andothersimple,basiccreditderivativeproductsusedtomanagecreditrisks.TheyareanaloguestoCreditDefaultSwap(CDS):

(1)CRMAisakindoffinancialcontractacceptedbybothbuyersandsellers.Withinacertainperiodinthefuture,buyersofcreditprotectionaresupposedtopaythecreditprotectionfeetocreditprotectionsellersaccordingtoagreedonstandardandprocedures,whilesellersoughttoprovidecreditriskprotectionserviceforbuyerswithregardtoagreedonobjectdebt.

(2)CRMWiscreatedbyinstitutionsoutsideofobjectentities,providescreditprotectionservicestoholdersregardingbondsorsimilarobjectdebt,andcancirculateonthemarket.Uptonow,researchonCRMinChinafocusesonpolicyresearch.ZhaiChenxi(2008)[9]hasdonetheoreticalcalculationofpricingofCDSproductsdenominatedinRMB,basedonapplicationofJarrow-TurnbullmodelinpricingofCDSproducts.ShiWenchao(2011)[10]byanalyzingthebackground,implicationandinstitutionalarrangementsofCRM,exploredtheconstructionoftheCRMmarketfromtheperspectivesofinstitutionalframeworkdesign,investorbuildup,marketmechanismandexternalenvironmentconstruction,creditriskpricing,aswellasinternationalcomparisonofCRMmarket,etc.

1.3Summary

Accordingtothesurveyabove,researchintheareaofcreditriskmitigationproductssuchasCDSandCRMathomeandabroadismostlyfocusedonproductdesign,mitigationeffects,capitalsupervisionandriskmanagement,etc,andrelativelyweakonproductpricingresearch..AndtheshorttimesincelaunchofCRM,CRMpricingbenchmarkinterestratesarestillnotperfect,thelackofbasicdatabasepricing,pricingmodelsandmethodsofresearchisstillinitsinfancy,themarketplayersandregulators,manyoftheirproblemsisnothigherrecognition.Therefore,thisarticletriestocombinethereleasestatusoftransactionpricingofCRMsinceCRMlaunchednearly6months,analysespricingfactorsofCRMcomprehensivelyandsystematically,andexploretheeffectivenessofJarrow-TurnbullmodelonCRMpricing,thenputforwardoptimizationmeasuresofCRMpricing.

2AnalysesonFactorsInfluencingCRMPricing

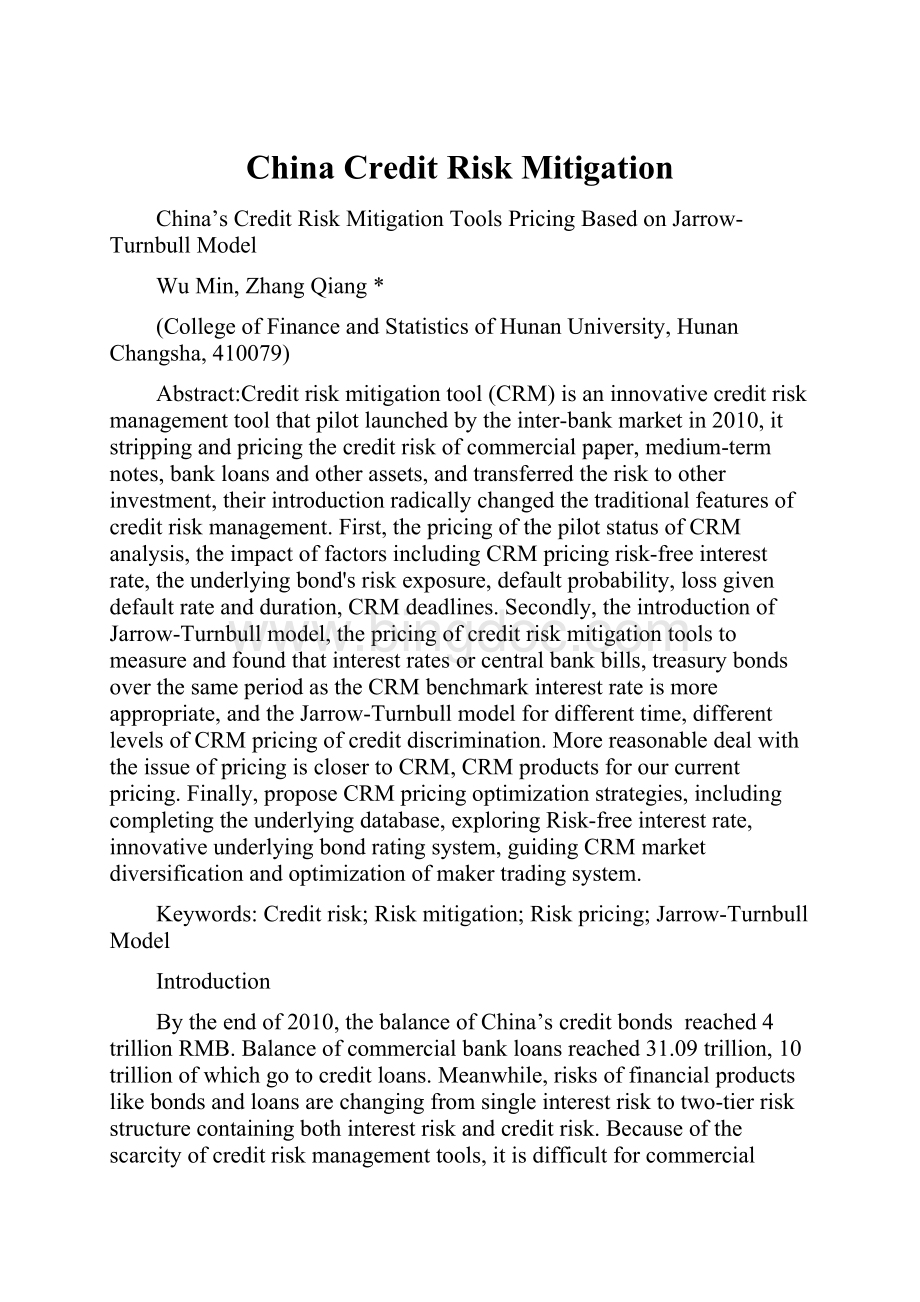

AsFigure1shows,CRMAiskindofafinancialcontractwithunderlyingmechanismlikethis:

buyersofcreditriskprotection,intheattempttopreventcrediteventsfromhappeningonthereferenceentity(objectbondscarryingcreditrisks),payafixedamountoffeesregularlytosellersofcreditriskprotection.Sellers,inreturn,providecreditriskprotectiontothebuyerswithregardtothereferenceentityinpredeterminedperiodoftime.BymeansofCRMtransaction,bothpartiescansuccessfullytransferandtransformcreditrisks.CRMWisdifferentfromCRMAinthatitisestablishedbyanindependentthirdparty,soneitherbuyersnorsellersneedtoholdanyreferenceentitybonds.

Fig.1.ThebasicprinciplesofCRMAdesign

TheunderlyingmechanismofCRMshowsthatthetheoreticalbaseforCRMpricingisthetheoryofdefaultprobabilityanddefaultlossrate,andisrelatedtoindexeslikeriskexposureofobjectbonds,defaultprobability,defaultlossrateandterms,etc.Fromtheprospectiveofmarketpricingmechanism,themajorityofmarketentitiesrelyonexistingobjectbondyieldcurves,andpriceusingsimplifiedcreditinterestratedifferencemethodsandbinarytreemethods.Orpricebyrisk-freeinterestratediscountafteradjustingliquiditypremium,onthebasisoftheinterestratedifferencebetweentheyieldcurveofbondswithsamecreditratingasCRMobjectbondsandtheyieldcurveoffinancialbondsornationaldebt(Shi,Wenchao,2011)[10].Meanwhile,accordingtotheinterestratetermstructuretheory(Hicks,1939)[11],thepriceoflong-termCRMishigherthanthatofshort-termCRMduetotheliquidityriskpremiumofCRM.Allinall,majorfactorsinfluencingCRMpricingincluderisk-freebenchmarkinterestrate,riskexposureofobjectbond,defaultprobability,de

升级会员

升级会员