亨格瑞管理会计英文第15版练习答案07.docx

《亨格瑞管理会计英文第15版练习答案07.docx》由会员分享,可在线阅读,更多相关《亨格瑞管理会计英文第15版练习答案07.docx(55页珍藏版)》请在冰点文库上搜索。

亨格瑞管理会计英文第15版练习答案07

CHAPTER7

COVERAGEOFLEARNINGOBJECTIVES

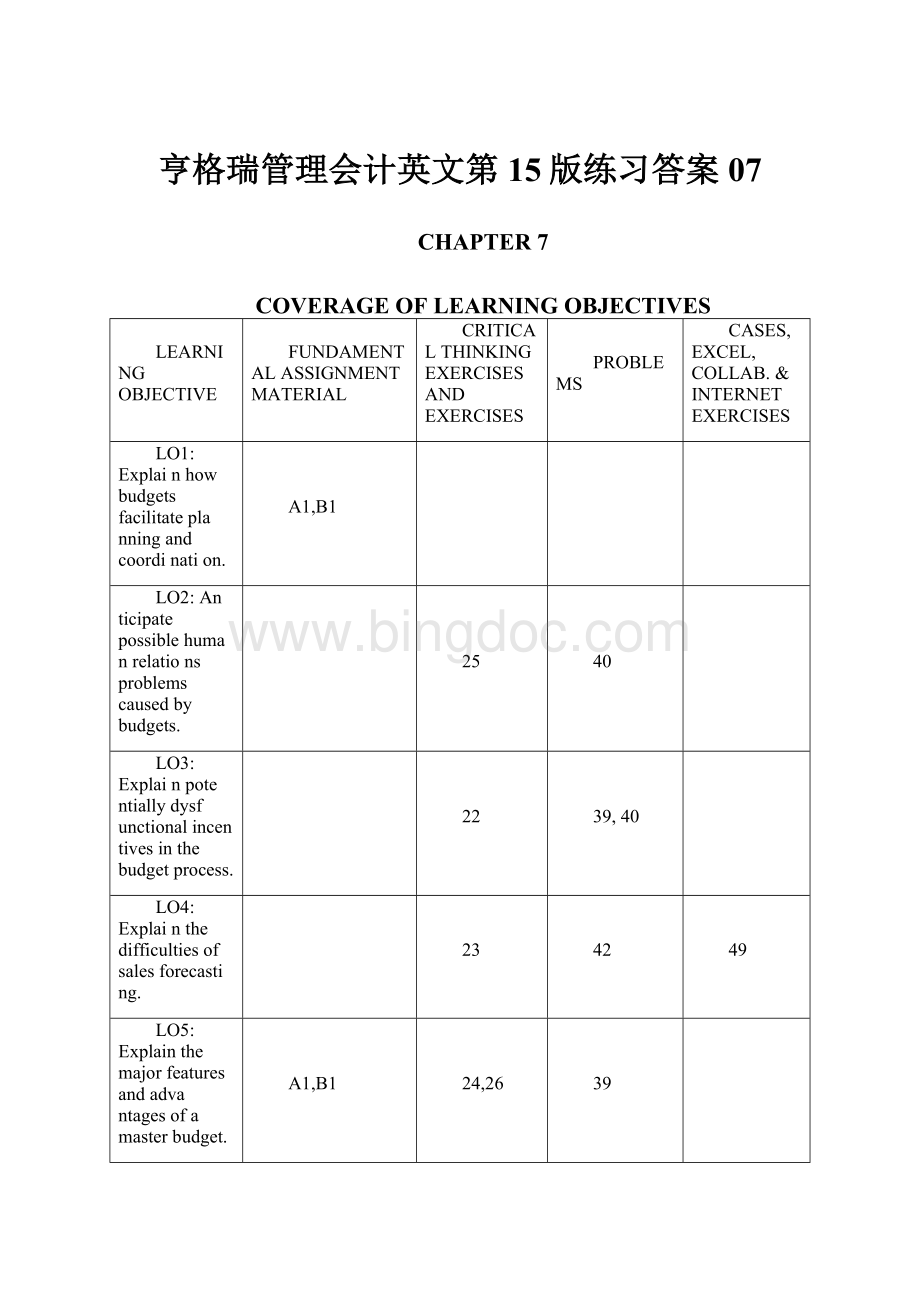

LEARNINGOBJECTIVE

FUNDAMENTALASSIGNMENTMATERIAL

CRITICALTHINKINGEXERCISESANDEXERCISES

PROBLEMS

CASES,EXCEL,COLLAB.&INTERNETEXERCISES

LO1:

Explainhowbudgetsfacilitateplanningandcoordination.

A1,B1

LO2:

Anticipatepossiblehumanrelationsproblemscausedbybudgets.

25

40

LO3:

Explainpotentiallydysfunctionalincentivesinthebudgetprocess.

22

39,40

LO4:

Explainthedifficultiesofsalesforecasting.

23

42

49

LO5:

Explainthemajorfeaturesandadvantagesofamasterbudget.

A1,B1

24,26

39

LO6:

Followtheprincipalstepsinpreparingamasterbudget.

A1,B1

29

40

43,45

LO7:

Preparetheoperatingbudgetandthesupportingschedules.

A1,B1

28,29,30,31

40

43,45,46,48

LO8:

Preparethefinancialbudget.

A1,B1

27,29,32,33,

34,35

36,37,38

43,44,47,48

LO9:

Useaspreadsheet

41,42

todevelopabudget(Appendix7).

CHAPTER7

IntroductiontoBudgetsandPreparingtheMasterBudget

7-A1(60-90min.)

1.ExhibitI

RAPIDBUYELECTRONICS,INC.

MallofAmericaStore

BudgetedIncomeStatement

FortheThreeMonthsEndingAugust31,20X8

Sales

$300,000

Costofgoodssold(.62x$300,000)

186,000

Grossprofit

$114,000

Operatingexpenses:

Salaries,wages,commissions

$60,000

Otherexpenses

12,000

Depreciation

1,500

Rent,taxesandotherfixedexpenses

33,000

106,500

Incomefromoperations.

$7,500

Interestexpense*

1,338

Netincome

$6,162

Seeschedulegforcalculationofinterest.

ExhibitII

RAPIDBUYELECTRONICS,INC.

MallofAmericaStore

CashBudget

FortheThreeMonthsEndingAugust31,20X8

June

July

August

Beginningcashbalanee

$5,800

$5,600

$5,079

Minimumcashbalaneedesired

5,000

5,000

5,000

(a)Availablecashbalanee

$800

$600

$79

Cashreceipts&disbursements:

Collectionsfromcustomers

(scheduleb)

$75,200

$121,400

$90,800

Paymentsformerchandise

(scheduled)

(86,800)

(49,600)

(49,600)

Fixtures(purchasedinMay)

(11,000)

-

-

Paymentsforoperating

expenses(schedulef)

(44,600)

(30,200)

(30,200)

(b)Netcashreceipts&disbursements

$(67,200)

$41,600

$11,000

Excess(deficiency)ofcashbefore

financing(a+b)

(66,400)

42,200

11,079

Financing:

Borrowing,atbeginningofperiod

$67,000$

-$-

Repayment,atendofperiod

-

(41,000)

(10,000)

Interest,10%perannum

-

(1,121)*

(217)*

(c)Totalcashincrease(decrease)

fromfinancing

$67,000

$(42,121)

$(10,217)

(d)Endingcashbalanee(beginning

balanee+b+c)

$5,600

$5,079

$5,862

Seescheduleg

ExhibitIII

RAPIDBUYELECTRONICS,INC.MallofAmericaStoreBudgetedBalaneeSheet

Assets

August31,20X8

Cash(ExhibitII)

$5,862

Accountspayable

$37,200

Accountsreceivable*

86,400

Notespayable

16,000**

Merchandiseinventory

37,200

Totalcurrentliabilities

$53,200

Totalcurrentassets

$129,462

Netfixedassets:

Owners'equity:

$33,600less

$102,200plusnet

depreciationof$1,500

32,100

incomeof$6,162

108,362

Totalassets

$161,562

Totalequities

$161,562

*Julysales,20%x

90%x$80,000

$14,400

Augustsales,100%

x90%x$80,000

72,000

Accountsreceivable

$86,400

**Seescheduleg

LiabilitiesandOwnersEquity

JulyAugustTotal

$72,000$270,000

8,00030,000

$80,000$300,000

Desiredpurchases:

62%xnextmonth'ssales$86,800

$49,600

$49,600

$37,200

Scheduled:

DisbursementsforPurchases

June

July

August

Lastmonth'spurchases(toExhibitII)

$86,800

$49,600

$49,600

Otherrequireditemsrelatedtopurchases

Accountspayable,August31,2008

(62%xSeptembersales-toExhibitIII)Costofgoodssold(toExhibitI)

$86,800

$49,600

$37,200

$49,600

Schedulee:

OperatingExpenseBudget

June

July

August

Total

Salaries,wages,commissions

$28,000

$16,000

$16,000

$60,000

OtherVariableexpenses

5,600

3,200

3,200

12,000

Fixedexpenses

11,000

11,000

11,000

33,000

Depreciation

500

500

500

1,500

Totaloperatingexpenses

$45,100

$30,700

$30,700

$106,500

Schedulef:

PaymentsforOperatingExpenses

June

July

August

Variableexpenses

$33,600

$19,200

$19,200

Fixedexpenses

11,000

11,000

11,000

Totalpaymentsforoperatingexpenses

$44,600

$30,200

$30,200

Scheduleg:

Interestcalculations

June

July

August

Beginningbalanee

$67,000

$67,558

$26,000

Monthlyinterestexpense@10%

558

563

217

Endingbalaneebeforerepayment

$67,558

68,121

26,217

Principalrepayment(from

statementofreceiptsanddisbursements)

(41,000)

(10,000)

Interestpayment

(1,121)

(217)

Endingbalanee

$26,000

$16,000

2.Thisisanexampleoftheclassicshort-term,self-liquidatingloan.

Theneedforsuchaloanoftenarisesbecauseoftheseasonalnatureofabusiness.Thebasicsourceofcashisproceedsfromsalestocustomers.Intimesofpeaksales,thereisalagbetweenthesaleandthecollectionofthecash,yetthepayrollandsuppliersmustbepaidincashrightaway.Whenthecashiscollected,itinturnmaybeusedtorepaytheloan.Theamountoftheloanandthetimingoftherepaymentareheavilydependentonthecredittermsthatpertaintoboththepurchasingandsellingfunctionsofthebusiness.

7-B1(60-120min.)$referstoAustraliandollars.

1.SeeExhibitsI,II,andIIIandsupportingschedulesa,b,c,d.

2.Thecashbudgetandbalaneesheetclearlyshowthebenefitsofmovingtojust-in-timepurchasing(thoughthetransitionwouldrarelybeaccomplishedaseasilyasthisexamplesuggests).However,thecompanywouldbenobetteroffifitleftmuchofitscapitaltiedupincash--ithasmerelysubstitutedoneassetforanother.Ataminimum,theexcesscashshouldbeinaninterestbearingaccount--theinterestearnedorforgoneisoneofthecostsofinventory.

$156,200

50,000

$24,000

124,000

$24,000$24,000

140,00076,000

$206,200

64,000

$148,000

156,200

$164,000$100,000

32,20024,000

$142,200$

-

$131,800$76,000

DecemberJanuaryFebruaryMarch

Schedulec:

PurchasesBudget

ExhibitI

WALLABYKITE

CashBudget

FortheThreeMonthsEndingMarch31,20X2

JanuaryFebruaryMarch

Cashbalanee,beginning

$20,000

$20,400

$138,767

Minimumcashbalaneedesired

20,000

20,000

20,000

(a)

Availablecashbalanee

0

400

118,767

Cashreceiptsanddisbursements:

Collectionsfromcustomers(Scheduleb)

Paymentsformerchandise

188,800

252,400

200,000

(Scheduled)

(142,200)

-

(131,800)

Rent

(32,200)

(1,000)

(1,000)

Wagesandsalaries

(60,000)

(60,000)

(60,000)

Miscellaneousexpenses

(10,000)

(10,000)

(10,000)

Dividends

Purchaseoffixtures

(6,000)

-

(12,000)

(b)

Netcashreceipts&disbursementsExcess(deficiency)ofcash

$(61,600)

$181,400

$(14,800)

beforefinancing(a+b)

Financing:

$(61,600)

$181,800

$103,967

Borrowing,atbeginningofperiod

$62,000$

-$-

Repayment,atendofperiod

-

(62,000)

Simpleinterest,10%monthly

-

(1,033)

(c)

Totalcashincrease(decrease)

fromfinancing

$62,000

$(63,033)$

-

(d)

Cashbalanee,end(beginning

balanee+c+b)

$20,400

$138,767

$123,967

ExhibitII

WALLABYKITE

BudgetedIncomeStatement

FortheThreeMonthsEndingMarch31,20X2

Sales(Schedulea)

$680,000

Costofgoodssold(Schedulec)

340,000

Grossmargin

$340,000

Operatingexpenses:

Rent*

$67,000

Wagesandsalaries

180,000

Depreciation.

3,000

Insuranee

1,500

Miscellaneous

30,000

281,500

Netincomefromoperations

$58,500

Interestexpense

1,033

Netincome

$57,467

*(January-Marchsalesless$4

0,000)x.10plus3

x$1,000

Exhibit山WALLABYKITE

BudgetedBalaneeSheet

March31,20X2

Assets

Currentassets:

Totalliabilitiesandstockholders'equity.

*Februarysales(.10x$280,000)plusMarchsales(.40x$152,000)$88,800

**Balanee,December31,20X1$102,800

Add:

Netincome57,467

Total$160,267

Less:

Dividendspaid6,000

Balanee,March31,20X2$154,267

7-1Budgeting1)providesanopportunityformanagerstoreevaluateexistingactivitiesandevaluatepossiblenewactivities,2)compels

managerstothinkaheadbyformalizingtheirresponsibilitiesforplanning,3)aidsmanagersincommunicatingobjectivestounitsandcoordinatingactionsacrosstheorganization,and4)provides

benchmarkstoevaluatesubsequentperformanee.

7-2Budgetingisprimarilyattentiondirectingbecauseithelps

managerstofocusonoperatingorfinancialproblemsearlyenoughforeffectiveplanningoraction.

7-3Strategicplanningcoversnospecifictimeperiod,isquitegeneral,andoftenisnotbuiltaroundfinancialstatements.Long-rangeplanningusuallyhasa5-or10-yearhorizonandconsistsoffinancialstatementswithoutmuchdetail.Budgetingusuallyhasahorizonofoneyearorless,andconsistsoffinancialstatementswithmuchdetail.

7-4Continuousbudgetsaddamonth(orquarter)inthefutureasthe

month(orquarter)justendedisdropped.Therefore,thecontinuousbudgetprovidesacontinuallyupdatedbudgetlookingtwelvemonthsahead.Whenthenewmonth(orquarter)isadded,thebudgetfortheremainderofthecurrentyearmayalsoberevised.Whencompaniesrevisethebudgetsfortheremainderofthecurrentyear,theyusuallycomparesubsequentresultstotheoriginalbudget(afixedtarget)inaddit

升级会员

升级会员