第十五版710章答案.docx

《第十五版710章答案.docx》由会员分享,可在线阅读,更多相关《第十五版710章答案.docx(36页珍藏版)》请在冰点文库上搜索。

第十五版710章答案

CHAPTER7

COVERAGEOFLEARNINGOBJECTIVES

CHAPTER7

IntroductiontoBudgetsandPreparingtheMasterBudget

7-A1(60-90min.)

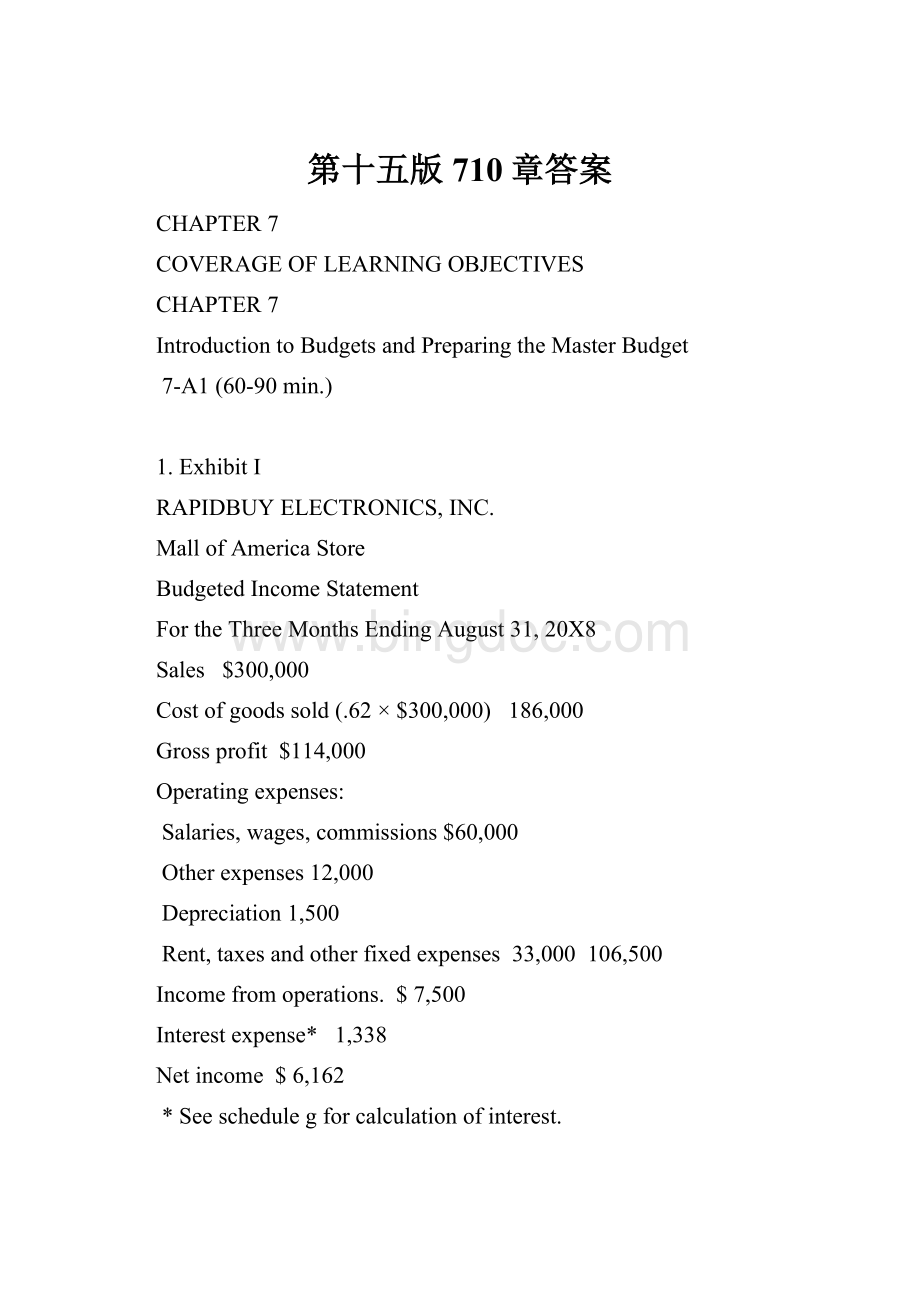

1.ExhibitI

RAPIDBUYELECTRONICS,INC.

MallofAmericaStore

BudgetedIncomeStatement

FortheThreeMonthsEndingAugust31,20X8

Sales$300,000

Costofgoodssold(.62×$300,000)186,000

Grossprofit$114,000

Operatingexpenses:

Salaries,wages,commissions$60,000

Otherexpenses12,000

Depreciation1,500

Rent,taxesandotherfixedexpenses33,000106,500

Incomefromoperations.$7,500

Interestexpense*1,338

Netincome$6,162

*Seeschedulegforcalculationofinterest.

ExhibitII

RAPIDBUYELECTRONICS,INC.

MallofAmericaStore

CashBudget

FortheThreeMonthsEndingAugust31,20X8

JuneJulyAugust

Beginningcashbalance$5,800$5,600$5,079

Minimumcashbalancedesired5,0005,0005,000

(a)Availablecashbalance$800$600$79

Cashreceipts&disbursements:

Collectionsfromcustomers

(scheduleb)$75,200$121,400$90,800

Paymentsformerchandise

(scheduled)(86,800)(49,600)(49,600)

Fixtures(purchasedinMay)(11,000)--

Paymentsforoperating

expenses(schedulef)(44,600)(30,200)(30,200)

(b)Netcashreceipts&disbursements$(67,200)$41,600$11,000

Excess(deficiency)ofcashbefore

financing(a+b)(66,400)42,20011,079

Financing:

Borrowing,atbeginningofperiod$67,000$-$-

Repayment,atendofperiod-(41,000)(10,000)

Interest,10%perannum-(1,121)*(217)*

(c)Totalcashincrease(decrease)

fromfinancing$67,000$(42,121)$(10,217)

(d)Endingcashbalance(beginning

balance+b+c)$5,600$5,079$5,862

*Seescheduleg

ExhibitIII

RAPIDBUYELECTRONICS,INC.

MallofAmericaStore

BudgetedBalanceSheet

August31,20X8

AssetsLiabilitiesandOwners’Equity

Cash(ExhibitII)$5,862Accountspayable$37,200

Accountsreceivable*86,400Notespayable16,000**

Merchandiseinventory37,200Totalcurrentliabilities$53,200

Totalcurrentassets$129,462

Netfixedassets:

Owners'equity:

$33,600less$102,200plusnet

depreciationof$1,50032,100incomeof$6,162108,362

Totalassets$161,562Totalequities$161,562

*Julysales,20%×90%×$80,000$14,400

Augustsales,100%×90%×$80,00072,000

Accountsreceivable$86,400

**Seescheduleg

JuneJulyAugustTotal

Schedulea:

SalesBudget

Creditsales(90%)$126,000$72,000$72,000$270,000

Cashsales(10%)14,0008,0008,00030,000

Totalsales(toExhibitI)$140,000$80,000$80,000$300,000

Scheduleb:

CashCollections

JuneJulyAugust

Cashsales$14,000$8,000$8,000

Onaccountsreceivablefrom:

Aprilsales10,800--

Maysales50,40012,600-

Junesales-100,80025,200

Julysales--57,600

Totalcollections(toExhibitII)$75,200$121,400$90,800

Schedulec:

PurchasesBudgetMayJuneJulyAugust

Desiredpurchases:

62%×nextmonth'ssales$86,800$49,600$49,600$37,200

Scheduled:

DisbursementsforPurchasesJuneJulyAugust

Lastmonth'spurchases(toExhibitII)$86,800$49,600$49,600

Otherrequireditemsrelatedtopurchases

Accountspayable,August31,2008

(62%×Septembersales-toExhibitIII)$37,200

Costofgoodssold(toExhibitI)$86,800$49,600$49,600

Schedulee:

OperatingExpenseBudget

JuneJulyAugustTotal

Salaries,wages,commissions$28,000$16,000$16,000$60,000

OtherVariableexpenses5,6003,2003,20012,000

Fixedexpenses11,00011,00011,00033,000

Depreciation5005005001,500

Totaloperatingexpenses$45,100$30,700$30,700$106,500

Schedulef:

PaymentsforOperatingExpenses

JuneJulyAugust

Variableexpenses$33,600$19,200$19,200

Fixedexpenses11,00011,00011,000

Totalpaymentsforoperatingexpenses$44,600$30,200$30,200

Scheduleg:

Interestcalculations

JuneJulyAugust

Beginningbalance$67,000$67,558$26,000

Monthlyinterestexpense@10%558563217

Endingbalancebeforerepayment$67,55868,12126,217

Principalrepayment(from

statementofreceiptsanddisbursements)(41,000)(10,000)

Interestpayment(1,121)(217)

Endingbalance$26,000$16,000

2.Thisisanexampleoftheclassicshort-term,self-liquidatingloan.Theneedforsuchaloanoftenarisesbecauseoftheseasonalnatureofabusiness.Thebasicsourceofcashisproceedsfromsalestocustomers.Intimesofpeaksales,thereisalagbetweenthesaleandthecollectionofthecash,yetthepayrollandsuppliersmustbepaidincashrightaway.Whenthecashiscollected,itinturnmaybeusedtorepaytheloan.Theamountoftheloanandthetimingoftherepaymentareheavilydependentonthecredittermsthatpertaintoboththepurchasingandsellingfunctionsofthebusiness.

7-25Akeytoemployeeacceptanceofabudgetisparticipation.Budgetscreatedwiththeactiveparticipationofallaffectedemployeesaregenerallymoreeffectivethanbudgetsimposedonsubordinates.Ifabudgetistohelpdirectfutureactivities,employeesmustacceptthebudget.Acceptancemeansbelievingthatthebudgetreflectsadesiredfuturepathfortheorganization.Ifamanagerhasbeenaparticipantindeterminingthefuturepath–thatis,helpeddevelopthebudget–heorsheismorelikelytoacceptitasadesirableobjective.

7-36(20-25min.)ThecollectionsfromMarchsalesareabittricky.NotethatthereceivablebalancefromMarchsalesatMarch31is$450,000;therefore,fourfifths(because40/50willbecollectedinApriland10/50willbecollectedinMay)willbereceivedinApril.

MERRILLNEWSANDGIFTS

BudgetedStatementofCashReceiptsandDisbursements

FortheMonthEndingApril30,20X7

Cashbalance,March31,20X7$100,000

Addreceipts,collectionsfromcustomers:

FromAprilsales,1/2×$1,000,000$500,000

FromMarchsales,4/5×$450,000360,000

FromFebruarysales80,000940,000

Totalcashavailable$1,040,000

Lessdisbursements:

Merchandisepurchases,$450,000×40%$180,000

Paymentonaccountspayable460,000

Payrolls90,000

Insurancepremium1,500

Otherexpenses45,000

Repaymentofloanandinterest97,200873,700

Cashbalance,April30,20X7$166,300

7-40(25-30min.)

1.Anoptimisticpreliminarybudgetmightbeasfollows,assuminglevelsalesvolume,a$.94perpoundprice,anda2%decreaseinvariablecosts.

Sales,1.6millionpounds@$.94/pound$1,504,000

Variablecosts(862,400)

Fixedcosts,primarilydepreciation(450,000)

Pretaxprofit$191,600

Thisbudgetdoesnotmeetthe$209,000profitgoal.StarkhasadilemmaofsubmittingarealisticbudgetthatdoesnotmeetPhilp'sgoalorpreparinganunrealisticbudget.Thefollowingbudget,whichassumesthatpriceswillnotfall,saleslevelswillbemaintained,andsomefixedcostswillbesaved,wouldmeettheprofittarget.AlthoughStarkdoesnotbelievetheassumptions,shemightfeelpressuretosubmitit(orsomethingsimilar)toheadquarters:

Sales,1.6millionpounds@$.95/pound$1,520,000

Variablecosts,.98×$880,000(862,400)

Fixedcosts,primarilydepreciation(448,600)*

Pretaxprofit$209,000

*$1,520,000-$862,400-$209,000

2.Twomajorproblemsarethearbitrarysettingofbudgettargetsbytopmanagementwithoutregardtowhetherthetargetscanbeachievedandthedraconianmeasuresusedwhenabudgetisnotmet,eveniftheshortfallissmallorreasonableexplanationsfortheshortfallaregiven.

3.Apparentlythepreliminaryfinancialresultsareasfollows:

Sales,1.6millionpounds@$.945/pound$1,512,000

Variablecosts,.98×$880,000(862,400)

Fixedcosts,primarilydepreciation(450,000)

Pretaxprofit$199,600

Extendingthedepreciablelivesoffixedassetsby2yearscouldincreasethisprofitby$15,000to$214,600,wellabovethetarget.Butdoingsowouldbemanipulatingtheaccountingsystemtoachievedesirableresults.Whentheestimatesofdepreciableliveswerefirstmade,theremayhavebeenmuchuncertaintyintheestimates.However,changingtheaccountingmethodtomakethefinancialresultslookbetterisanethicalviolation.

Managersshouldnotchangeaccountingmethodsjusttomaketheirperformancelookbetter(orinthiscase,tosavetheirjob).Althoughchangingthedepreciationscheduleisnotethical,itiseasytoseehowthebudgetingprocesscreatesanincentiveforsuchunethicalbehavior.Ifthebudgetandreportingprocessmakesexcellentperformanceappeardeficient,theremaybegreattemptationformanagerstocheatthesystem.

7-43(80-100min.)

1.OnJanuary1,SaltLakeLightOperaneedstoborrow$2,057,000,onApril1itneedsanadditional$562,000,onSeptember31itcanrepay$2,014,000,butonOctober1itmustagainborrow$726,000.Thiscanbeseenfromthefollowinganalysis(inthousandsofdollars):

Qtr.1Qtr.2Qtr.3Qtr.4

Beginningcashbalance208200200200

Minimumcashbalancedesired200200200200

Availablecashbalance8000

Cashreceipts&disbursement:

Collectionsfromcustomers

(1)8831,8934,5042,024

Paymentsforsupplies

(2)(780)(200)

Otherexpenses(3)(30)(30)(30)(30)

Paymentsforpayroll(4)(2,046)(2,100)(2,100)(2,100)

Majorequipment(5)(100)(300)

Smallequipment(6)(60)(60)(60)(60)

Mortgageprincipal(7)(125)(125)

Mortgageinterest(8)(140)(135)

Interestonworkingcapital(9)(32)

Netcashreceipts&disbursements(2,065)(562)2,014(726)

Excess(deficiency)ofcash

beforefinancing(2,057)(562)2,014(726)

Financing:

Borrowing(atbeginningofquarter)2,057562726

Repayment(atendofquarter)(2,014)

Totalcashincrease(decrease)

fromfinancing2,057

升级会员

升级会员